Big Four Loan Fraud Probe Expands as they Face AI Driven Document Manipulation Crisis

On 27 February, AFR reported that the Big Four fraud probe expanded as major banks reported suspected loan fraud to NSW Police, joining National Australia Bank and Commonwealth Bank in a widening investigation that now spans the entire big four. Police suspect that a single criminal network may have defrauded the major banks of at least $300 million. What began as a targeted inquiry has now evolved into a broader examination of mortgage applications, broker channels and lending controls across the sector.

This development marks more than a compliance review. The Big Four loan fraud investigation signals a structural challenge for Australian banking.

What the Big Four Loan Fraud Investigation Reveals About a $300 Million Multi Bank Network

Investigators believe the suspected fraudulent loans across institutions exceed $300 million. While some links have been identified to the Penthouse Syndicate, authorities expect the inquiry to expand beyond one group. As the Big Four loan fraud investigation widens, regulators and boards across the sector are reassessing their exposure to broker introduced applications.

According to AUSTRAC, criminals use mortgage structures to disguise the origin of illicit funds. By securing loans against real estate and repaying them with criminal proceeds, offenders convert dirty money into apparently legitimate wealth. As a result, the property market becomes a channel for money laundering rather than simple credit activity.

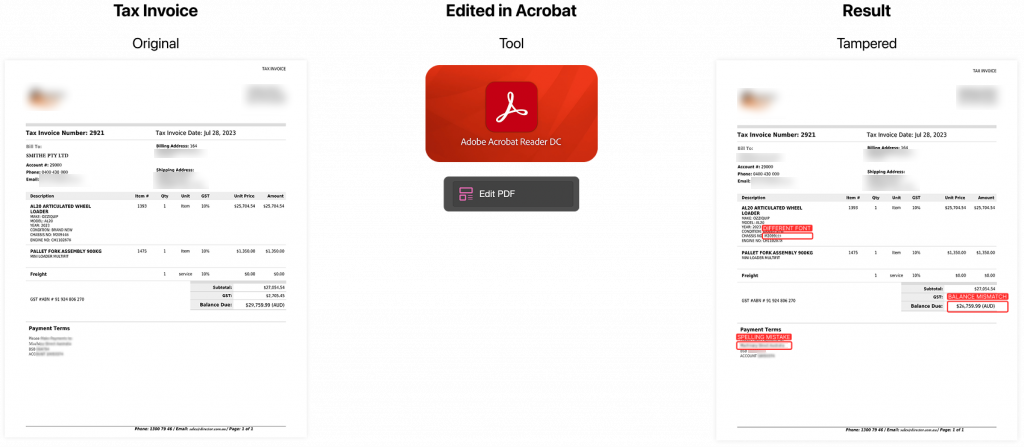

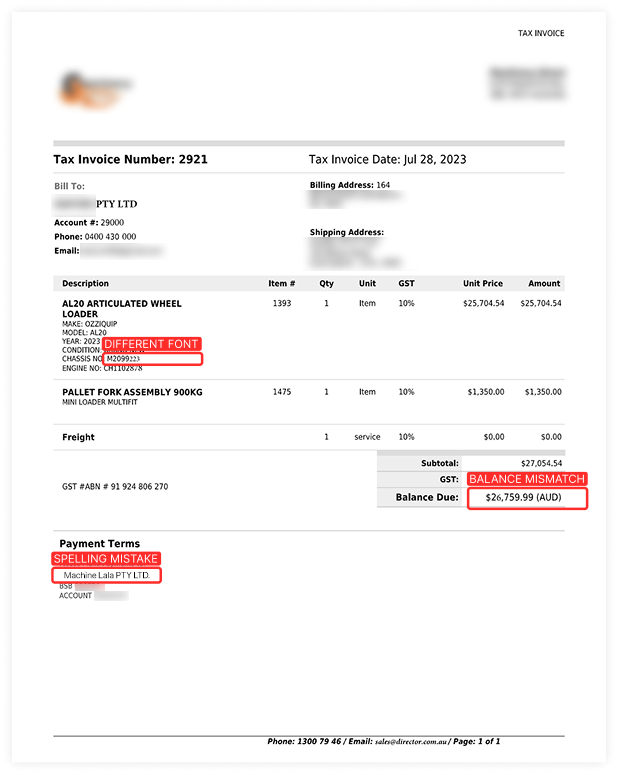

Authorities have identified several warning signs. Large overseas deposits exceed standard industry thresholds. Shell companies simulate trading history. Draft tax returns appear as income evidence despite not being lodged with the ATO. In addition, manipulated documents present internally consistent data that satisfies surface level checks.

The loans may perform. The repayments may continue. However, performance does not eliminate integrity risk. That is precisely why the Big Four loan fraud investigation has attracted such serious attention.

How Broker Channels, Shell Companies and Draft Tax Returns Expose Structural Vulnerabilities in Mortgage Origination

Broker and referral channels introduce complexity into the credit process. When intermediaries submit income documents and supporting records, banks rely on document authenticity before approval. Incentives can distort behaviour, particularly when commissions link directly to loan settlement.

Fraud networks understand these pressure points. They construct applications that appear logical and consistent. They align deposit amounts with serviceability calculations. They maintain repayment behaviour to avoid early detection. Consequently, the fraud remains hidden until deeper forensic review occurs.

The Big Four loan fraud investigation highlights a core weakness in this structure. Traditional verification focuses on visible content rather than digital structure.

Artificial Intelligence Is Now Weaponised in Mortgage Fraud and Legacy Controls Cannot Keep Pace

Artificial intelligence has lowered the barrier to document manipulation. Fraudsters now generate realistic payslips, alter bank statements, fabricate invoices and create synthetic identities using accessible AI tools. More importantly, they adjust metadata and formatting patterns to mimic legitimate documents.

Manual assessment and static OCR extraction systems cannot reliably detect these changes. Human reviewers cannot see hidden metadata edits or embedded object layers. As AI tools improve, the gap between fraud sophistication and traditional control environments widens.

Regulators have taken notice. ASIC has warned that AI misuse presents emerging risks to customers and market integrity. At the same time, expanded anti money laundering obligations will soon extend beyond banks to real estate agents, lawyers and conveyancers. Oversight is tightening. In this context, the Big Four loan fraud investigation may represent only the beginning of broader scrutiny.

Embedding Forensic AI Inside Lending Workflows to Detect Manipulated Applications Before Funds Are Released

This environment demands a shift from reactive review to proactive detection. Institutions must analyse not only what a document says but how it was created.

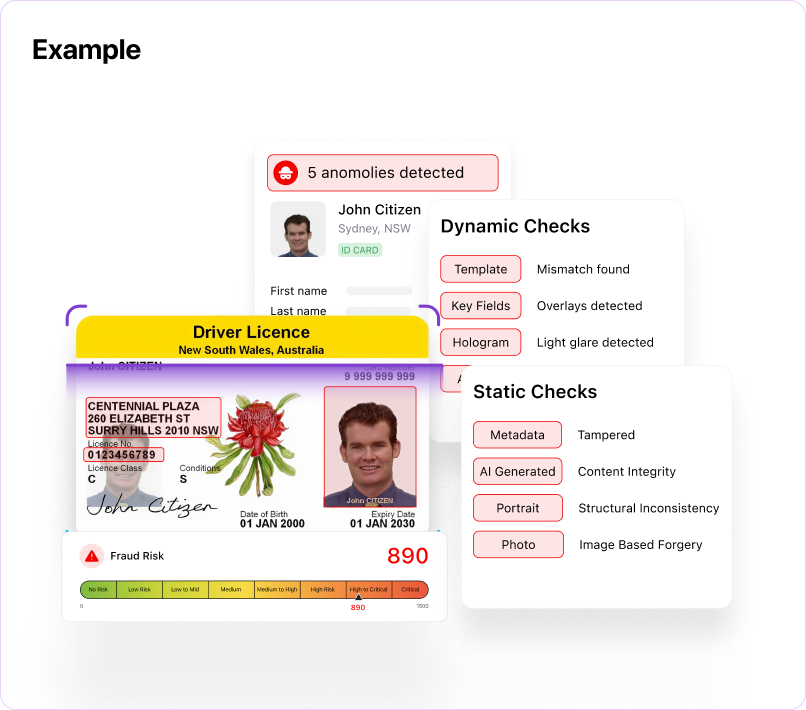

Fraud Check AI is DoxAI’s document fraud detection solution built to close this gap. It accelerates fraud detection, reduces manual review, and protects document integrity by analysing file structures, detecting manipulation, identifying inconsistencies, and verifying authenticity through advanced AI across three integrated layers of analysis.

1st Layer:

Static checks examine file structure, metadata, encoding signatures and hidden artefacts to determine whether manipulation has occurred.

2nd Layer:

Dynamic checks validate internal logic, including income calculations, date sequencing and cross document consistency.

3rd Layer:

Custom checks align directly with institutional risk parameters such as broker concentration, overseas deposit thresholds and unusual company structures.

Alfonso Porcelli, Chief Executive Officer of DoxAI, explains the urgency clearly.

“The expansion of the Big Four loan fraud investigation confirms that document fraud is engineered, not accidental. Fraud Check AI was built to detect structural manipulation before a loan reaches settlement. Institutions must assume that digital documents can be altered at scale and respond accordingly.”

He continues.

“Waiting for whistleblower complaints or post settlement audits increases regulatory exposure and reputational damage. Real time forensic validation inside origination workflows changes that equation.”mplaints or post settlement audits increases regulatory exposure and reputational damage. Real time forensic validation inside origination workflows changes that equation.”

Measurable Outcomes in Fraud Prevention

Fraud Check AI processes hundreds of millions of documents annually across financial services and regulated industries. In practice, it delivers three measurable benefits.

First, speed. Document verification can be up to 120 times faster than manual fraud analysis. This reduces backlogs in mortgage assessment and improves time to approval for genuine borrowers.

Second, cost efficiency. Automated fraud detection reduces reliance on large manual review teams, potentially achieving up to 50 times greater cost efficiency compared to purely human analysis.

Third, accuracy. Layered static, dynamic and custom checks significantly reduce fraud detection error rates, delivering up to 87 times fewer errors than manual review in tested scenarios.

Want to learn more about how Fraud Check AI can protect you from fraudulent document submissions?

The Fraud Check AI Defence That Works

DoxAI built Fraud Check AI specifically for Australia’s enterprise and regulatory landscape. It identifies synthetic identities, catches manipulated invoices, and prevents multi-million-dollar losses before approval.

DoxAI designed Fraud Check AI for Australia’s enterprise and regulatory environment, achieving SOC 2 Type 2, ISO 27001, GDPR, HIPAA and PCI DSS compliance while maintaining 99.97 per cent uptime with real time data replication across Australian data centres.

In a world where cyber threats evolve daily, reliability and compliance are a must.

Fraud Check AI Out of Box Categories

- Financial Statements

- Payslip

- Notice of Assessment

- Income Statements

- BAS Statements

- Credit Cards & Statements

- Bank Statements

- Invoices & Utility Bills

- Driving License

- Passports

- Insurance Documents

- Tax Returns

- Land Certificates

- Federal Issued Documents

- And 170+ more

Regulatory Escalation and Governance Risk for Australian Banks

The financial impact of suspected fraud captures headlines. However, the deeper issue involves governance and trust. When regulators question lending controls, scrutiny intensifies. When markets detect systemic weakness, investor confidence shifts.

Australia has already witnessed record penalties for anti money laundering failures. Consequently, boards now demand demonstrable assurance that fraud detection systems operate effectively and at scale. The expansion of the Big Four loan fraud investigation reinforces that expectation.

Banks must therefore strengthen controls not only to prevent credit losses but also to protect brand equity and regulatory standing.

Why Australian Banks Must Move From Post Settlement Audits to Real Time AI Driven Fraud Prevention

The Big Four loan fraud investigation underscores a broader reality. Fraud in mortgage lending evolves rapidly, particularly when supported by artificial intelligence. Institutions cannot rely solely on manual review and static verification processes.

Instead, they must embed forensic document analysis directly into credit assessment workflows. By detecting manipulated files before approval, banks reduce exposure to regulatory sanction, operational disruption and reputational harm.

Alfonso Porcelli summarises the imperative.

“AI now operates on both sides of the equation. Criminal networks deploy it to manipulate documents. Banks must deploy it to defend the integrity of their balance sheets.”

The investigation into the big four may expand further. Regardless of its final scope, one conclusion is clear. Fraud in 2026 is coordinated, sophisticated and technologically enabled. Therefore, prevention must be equally intelligent and equally automated.

If your organisation is reassessing mortgage and credit risk controls in light of the Big Four loan fraud investigation, now is the time to act. Let’s chat about how advanced AI driven fraud detection can strengthen your governance framework before the next investigation escalates further.

About DoxAI

DoxAI is your trusted process automation partner, enabling to transition from outdated systems to cutting-edge AI technology. Our platform streamlines the collection, management, processing, and storage of data, enhancing security, reducing operational costs, and boosting customer engagement. DoxAI empowers providers to automate and secure every step of their data and document handling processes. Our suite of products supports end-to-end workflows, from intake to archiving, ensuring privacy, compliance and faster service delivery.