CBA’s $1 Billion Fraud Probe Exposes AI Driven Document Manipulation in Australian Banking

On the 27th of February 2026, Commonwealth Bank reported itself to police and the corporate regulator over fears that about $1 billion in home loans (AFR, 2026). Banks may have obtained these loan originations using fraudulent documents, suspect deposits and shell companies. The review followed whistleblower complaints, scrutiny of broker introduced mortgages and heightened concern after the exposure of the Penthouse Syndicate, which allegedly defrauded National Australia Bank of around $150 million.

This is not an isolated compliance incident. It is a warning shot for the entire Australian banking industry. Fraudsters no longer rely only on forged payslips and inflated income statements in home loan applications. It now includes documents created or altered using artificial intelligence, draft tax returns submitted through accountants, shell companies that appear to have traded for years and deposits sourced from overseas channels that mask the origin of funds.

The scale matters. The sophistication matters more.

The Real Risk in the CBA Investigation

CBA has not suffered a financial loss because borrowers continue servicing many of the loans and the bank holds property as security. However, that misses the deeper issue. When a major bank identifies potential large-scale fraud in its loan book, three risks emerge.

First is regulatory exposure. If banks operate with inadequate systems and controls, regulators can impose enforcement action, penalties and ongoing compliance remediation. Australia has seen this before, including the $700 million penalty imposed on CBA in 2018 and Westpac’s $1.3 billion penalty in 2020 for anti-money laundering breaches.

Second is reputational damage. Trust Australian banks earn trust through strong governance and sound lending practices, but they can lose it quickly when failures occur. A perception that doctored applications, forged income documents and manipulated credit files can pass through lending processes undermines public confidence.

Operational time loss comes in third. Internal reviews, forensic audits, legal engagement, policy changes and regulator reporting consume thousands of hours of executive and compliance capacity. As a result, executives and compliance teams spend that time managing investigations instead of driving growth, innovation or improving customer experience.

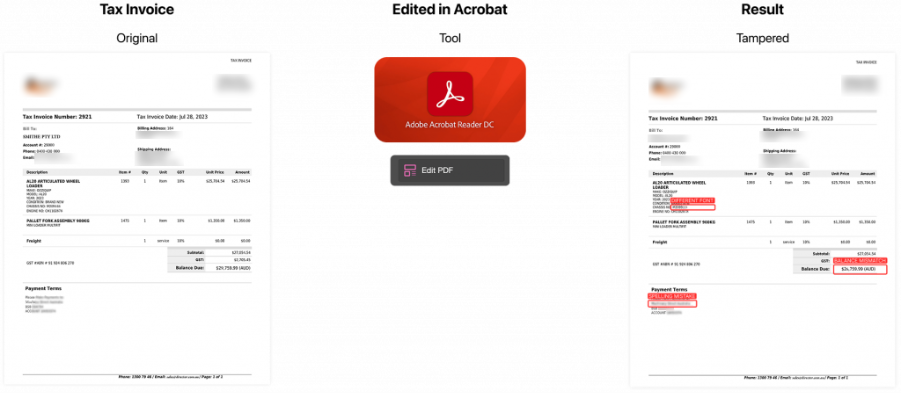

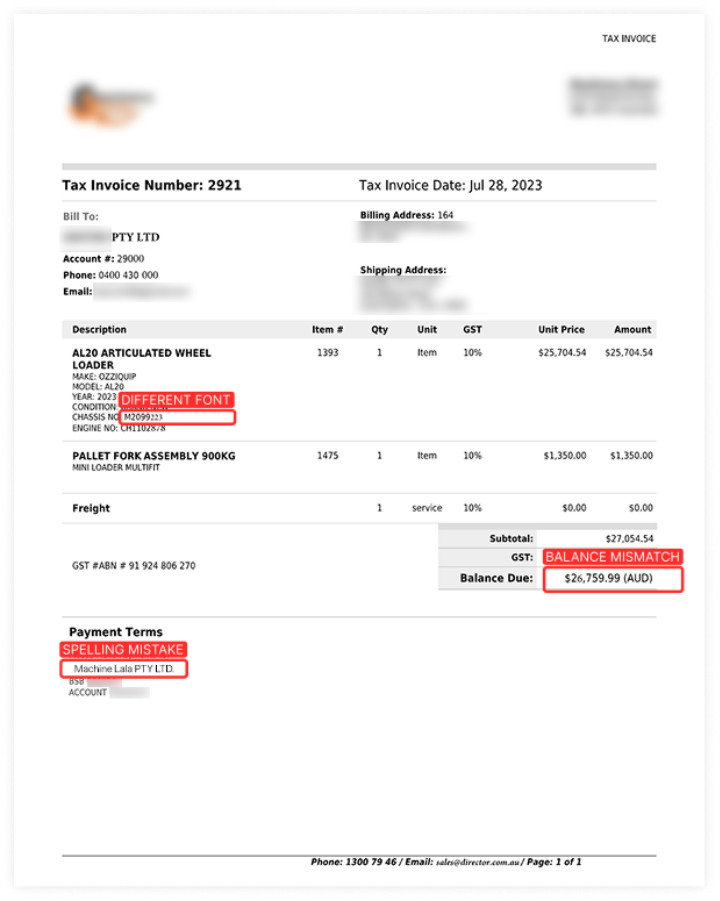

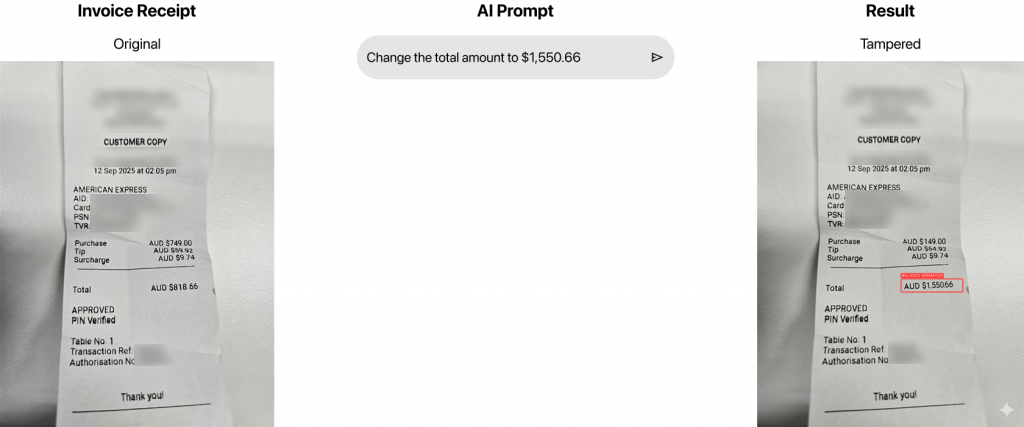

How Doctored Applications and AI Generated Documents Slip Through

The CBA probe reportedly focused on mortgages introduced by brokers and referrers such as real estate agents and accountants. Allegations include falsified income statements, draft tax returns, shell companies used to demonstrate trading history and overseas deposits used to meet lending thresholds.

Fraud specialists have warned that artificial intelligence is making it significantly easier to create authentic looking false documents. AI tools can generate near perfect income statements, payslips, invoices and identification documents in seconds. These documents can pass basic human review and even some legacy verification systems.

Traditional document verification often relies on manual review, static OCR extraction and checklist compliance. That approach assumes that a human can detect anomalies by sight. In 2026, that assumption is increasingly flawed.

The Weak Points in Lending Channels

The CBA case highlights several structural vulnerabilities in Australian banking.

Mortgage broking and referral channels introduce complexity. Incentives can distort behaviour. When brokers or accountants submit income documents, the bank depends heavily on their integrity and accuracy.

Fraudsters use shell companies that appear to have traded for two years to support business loan applications. They submit draft tax returns that they have not lodged with the ATO as evidence of income. They also understate living expenses and liabilities to improve serviceability.

When fraudsters organise their schemes carefully, they make documents look internally consistent. The deposit may be genuine in appearance. The property may secure the loan. Fraudsters can maintain repayments for months or years to avoid detection. The fraud only becomes visible when deeper analysis occurs or whistleblowers speak up.

This is where artificial intelligence driven fraud detection becomes essential.

AI Versus AI in Fraud Detection

Artificial intelligence is now used on both sides. Criminals use AI to create and manipulate documents. Banks must use AI to detect and prevent those manipulations.

Fraud detection in 2026 requires more than data extraction. It requires forensic analysis of file structure, metadata, embedded objects, logic consistency and cross dataset validation. It requires the ability to detect whether a document could exist in its current form.

How Fraud Check AI Could Have Mitigated the Risk

Fraud Check AI, developed by DoxAI, is designed specifically to address the types of risks highlighted in the CBA home loan investigation. It operates through three core layers.

Static Checks

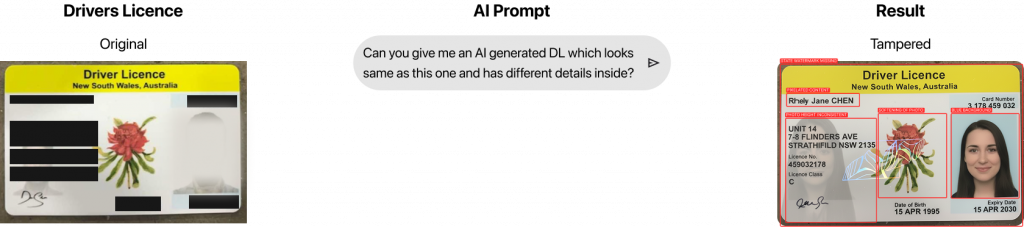

Static checks analyse the file itself. This includes metadata, timestamps, tool chains, embedded objects, fonts and encoding. If an income statement was generated using a generative AI tool, or if a tax return was edited shortly before submission, metadata may reveal inconsistencies.

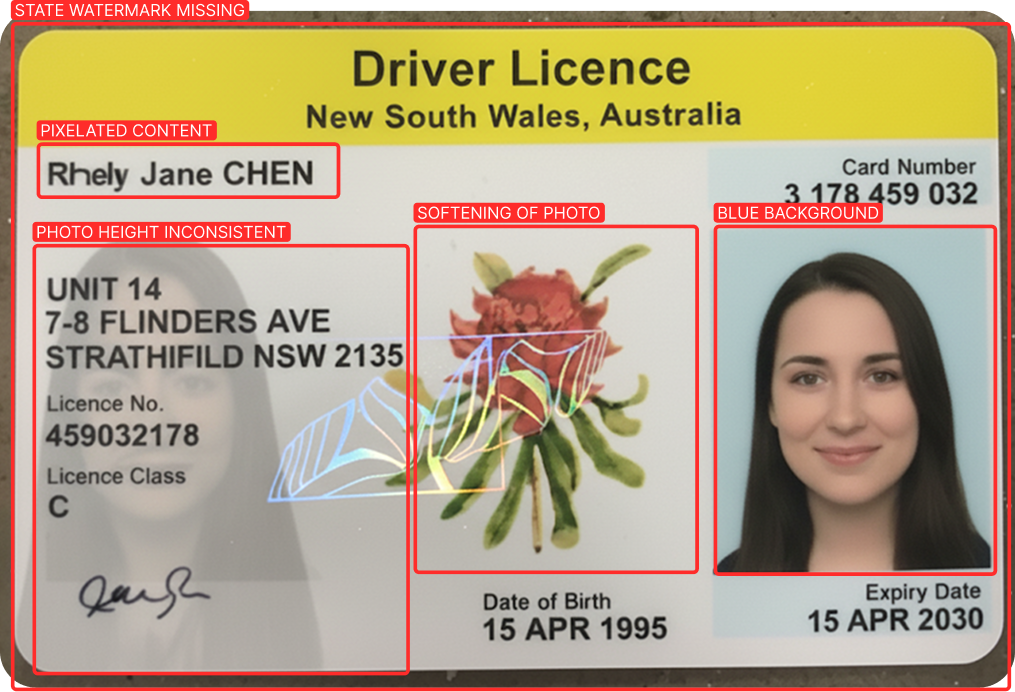

In the image below, Fraud Check AI identified an AI generated driver licence because the metadata indicated it was created using AI. In a lending context, similar checks could identify manipulated income documents or invoices.

Static checks answer the question: could this file exist this way.

Dynamic Checks

Dynamic checks validate the internal logic of the document. This includes arithmetic consistency, date logic, identity formats and cross field comparison.

In the CBA scenario, if a draft tax return overstated income, dynamic checks could compare declared income against bank statements, BAS statements or previous filings. If living expenses were understated, the system could identify inconsistencies across related documents.

Dynamic checks answer the question: does what is written actually make sense.

Custom Checks

Custom checks align to the bank’s specific credit policies and risk appetite. For example, thresholds around overseas deposits exceeding standard industry practice could trigger enhanced review. Repeat applicant patterns, broker concentration risk or unusual trust structures could be flagged automatically.

Custom checks answer the question: does this application meet our policy and risk parameters.

Want to see how it works? Book a free demo with our expert.

Measurable Outcomes in Fraud Prevention

Fraud Check AI processes hundreds of millions of documents annually across financial services and regulated industries. In practice, it delivers three measurable benefits.

First, speed. Document verification can be up to 120 times faster than manual fraud analysis. This reduces backlogs in mortgage assessment and improves time to approval for genuine borrowers.

Second, cost efficiency. Automated fraud detection reduces reliance on large manual review teams, potentially achieving up to 50 times greater cost efficiency compared to purely human analysis.

Third, accuracy. Layered static, dynamic and custom checks significantly reduce fraud detection error rates, delivering up to 87 times fewer errors than manual review in tested scenarios.

Want to learn more about how Fraud Check AI can protect you from fraudulent document submissions?

The Fraud Check AI Defence That Works

DoxAI built Fraud Check AI specifically for Australia’s enterprise and regulatory landscape. It identifies synthetic identities, catches manipulated invoices, and prevents multi-million-dollar losses before approval.

DoxAI designed Fraud Check AI for Australia’s enterprise and regulatory environment, achieving SOC 2 Type 2, ISO 27001, GDPR, HIPAA and PCI DSS compliance while maintaining 99.97 per cent uptime with real time data replication across Australian data centres.

In a world where cyber threats evolve daily, reliability and compliance are a must.

Fraud Check AI Out of Box Categories

- Financial Statements

- Payslip

- Notice of Assessment

- Income Statements

- BAS Statements

- Credit Cards & Statements

- Bank Statements

- Invoices & Utility Bills

- Driving License

- Passports

- Insurance Documents

- Tax Returns

- Land Certificates

- Federal Issued Documents

- And 170+ more

Beyond Money: Reputation and Regulatory Confidence

The $1 billion figure in suspected fraudulent home loans is headline grabbing. Yet the deeper issue is trust.

When regulators see repeated failures in anti-money laundering, credit assessment or document verification, scrutiny intensifies. When customers read about doctored applications and shell companies, confidence erodes.

Adopting advanced fraud detection technology is not only about reducing credit losses. It is about demonstrating to ASIC, AUSTRAC and shareholders that robust systems are in place. It is about protecting brand equity in a market where reputational damage spreads quickly.

The Future of Fraud Prevention in Australian Banking

The CBA investigation is unlikely to be the last of its kind. As artificial intelligence tools become more accessible, document manipulation and synthetic identity fraud will increase.

Australian banks must move from reactive review to proactive fraud prevention. This means embedding AI driven fraud detection into mortgage assessment, broker channels, trust lending and business loan origination.

Fraud Check AI represents a practical step in that direction. It does not replace human credit judgement. It strengthens it with forensic level analysis at scale.

The lesson from the CBA probe is clear. Fraud in lending is evolving. Systems must evolve faster. If banks can detect manipulated documents before approval, they can avoid not only financial loss, but regulatory sanction, operational disruption and reputational harm.

In 2026, fraudsters will attempt fraud. The real question is whether your systems can detect and stop it before it enters your loan book.

See the Future of Fraud Prevention

If your organisation is reassessing its lending controls in light of recent events, now is the time to act. Let’s chat about how advanced AI driven fraud detection can strengthen your risk management framework before the next headline emerges.

About DoxAI

DoxAI is your trusted process automation partner, enabling to transition from outdated systems to cutting-edge AI technology. Our platform streamlines the collection, management, processing, and storage of data, enhancing security, reducing operational costs, and boosting customer engagement. DoxAI empowers providers to automate and secure every step of their data and document handling processes. Our suite of products supports end-to-end workflows, from intake to archiving, ensuring privacy, compliance and faster service delivery.